Employer Health Plans and Generic Preferences: How Formularies Shape Your Prescription Costs

When you pick up a prescription at the pharmacy, you might not realize that the price you pay isn’t just about the drug itself-it’s shaped by a complex system your employer has signed up for. Most large employers offer prescription drug coverage, and nearly all of them use something called a formulary to decide which medications are covered and how much you’ll pay out of pocket. At the heart of this system is a clear, intentional preference: generic drugs.

Why Generics Are the Default Choice

Generic medications aren’t second-rate. The FDA confirms they contain the same active ingredients, work the same way, and are just as safe and effective as brand-name drugs. The big difference? Price. Generics typically cost 80-85% less than their brand-name equivalents. That’s not a guess-it’s backed by data. According to the Schauer Group, generic drugs save more than $3 billion every week in the U.S. That’s over $150 billion a year. Employers don’t choose generics because they’re cheap for the sake of it. They choose them because they’re the most effective way to keep health plan costs under control. When a brand-name drug’s patent expires, a generic version enters the market. That’s when the system kicks in. Pharmacy Benefit Managers (PBMs)-the middlemen that manage drug coverage for most employer plans-automatically move the generic to the lowest cost tier. The brand-name version? It gets bumped up, often to the highest tier, where you pay significantly more.How Formulary Tiers Work

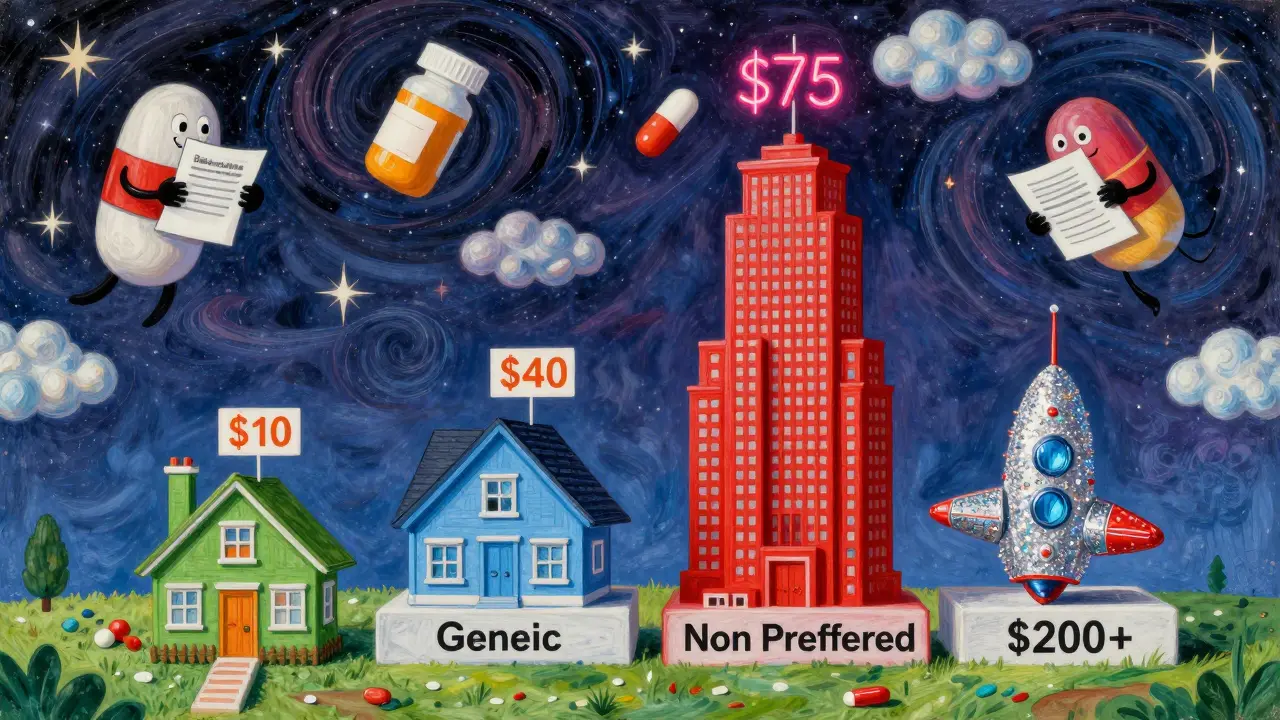

Most employer plans use a tiered system to divide medications into cost categories. Here’s how it usually breaks down:- Tier 1 (Generic): $10 copay. This is where most prescriptions start. If your drug has a generic version, this is the default.

- Tier 2 (Preferred Brand): $40 copay. These are brand-name drugs that the plan still covers, usually because there’s no generic yet or because they’re considered clinically better than other brands.

- Tier 3 (Non-Preferred Brand): $75 copay. These are brand-name drugs with available generics. If you choose the brand instead of the generic, you pay more.

- Tier 4 (Specialty): $200+ or coinsurance (e.g., 30% of cost). These are high-cost drugs for complex conditions like cancer, MS, or rheumatoid arthritis.

These numbers aren’t universal-they vary by plan-but the structure is. For example, in Ohio, the Department of Administrative Services uses this exact tier system for state employer plans. If you’re on a chronic condition like diabetes or high blood pressure, your drug is likely in Tier 1. If you’re on a newer brand-name drug with no generic, it might be in Tier 2. But if you insist on the brand when a generic is available? You’re moving up the ladder-and paying more.

Who Controls What’s Covered?

Behind the scenes, three companies control most employer prescription coverage: OptumRx, CVS Caremark, and Express Scripts. Together, they manage drug benefits for the majority of Americans with employer-sponsored insurance. These PBMs don’t just set tiers-they decide what stays on the formulary at all. In January 2024, each of these three PBMs removed over 600 drugs from their formularies. That’s more than 1,800 medications gone in one move. Why? It’s negotiation. PBMs use exclusions as leverage. If a drugmaker won’t offer a big enough discount, the PBM drops the drug. That forces the manufacturer to either lower prices or risk losing access to millions of patients. But here’s the catch: the savings from these negotiations don’t always reach you. PBMs use a pricing model called gross-to-net (GTN). That means a drug might have a list price of $100, but after rebates, discounts, and returns, the PBM nets only $45. The average GTN spread is 55%. That’s $55 of savings that never shows up on your copay receipt. The system saves money overall-but you might not see it.What You Can Do

You don’t have to guess how your coverage works. Here’s how to take control:- Check your insurer’s website. Look for your plan’s drug list. It’s often called a “formulary” or “drug list.”

- Review your Summary of Benefits and Coverage (SBC). It’s required by law and explains your copays and coverage rules.

- Ask your pharmacist. They know what’s covered and what’s cheaper. If your prescription is expensive, ask: “Is there a generic?”

- Call your insurer. If your drug was dropped from the formulary or moved to a higher tier, you can request a coverage exception. Your doctor can help with this.

Many employees are willing to use generics-they just don’t know they can. Employers who communicate clearly-through emails, payroll inserts, or even text messages-see higher generic use and lower overall drug spending. If your employer doesn’t explain this, ask them to. Knowledge is your best tool.

What Happens When Your Drug Disappears

It’s not rare for a medication to be removed from your plan’s formulary. Maybe the PBM cut a deal with a competitor. Maybe a generic just came out. Either way, you might show up at the pharmacy one day and find your drug isn’t covered anymore. Don’t panic. You have options:- Switch to the generic version (if available).

- Ask your doctor for an alternative drug that’s still on formulary.

- File a coverage exception. Your doctor can submit paperwork saying the drug is medically necessary. If approved, your plan will cover it-even if it’s off-formulary.

Some employers even offer care management programs. These programs assign a health coach who can help you find lower-cost alternatives, apply for patient assistance programs, or navigate appeals. If your plan offers this, use it.

The Bigger Picture

The system is designed to save money. And it works-on paper. Generics are cheaper. Formularies push people toward them. PBMs negotiate big discounts. But the gap between what’s saved and what you pay remains wide. The $150 billion saved annually doesn’t always translate to lower premiums or copays for you. The future of employer drug coverage will likely see more exclusions, more tiered structures, and more pressure on manufacturers. But the goal stays the same: get you on the cheapest effective drug possible. And that drug? It’s almost always the generic.So next time you’re handed a prescription, ask: Is there a generic? And if the answer is yes-you’re not just saving money. You’re using the system the way it was designed to work.

Why are generic drugs so much cheaper than brand-name drugs?

Generic drugs are cheaper because they don’t need to repeat expensive clinical trials. The original brand-name drug already proved safety and effectiveness. Generic manufacturers only need to show their version is bioequivalent-meaning it works the same way in the body. Without the cost of research, marketing, and advertising, generics can be sold at 80-85% less than the brand version.

Are generic drugs as safe and effective as brand-name drugs?

Yes. The FDA requires generics to meet the same strict standards as brand-name drugs. They must have the same active ingredient, strength, dosage form, and route of administration. They’re tested for quality and performance. Millions of people use generics every day without issue. The FDA states they are as safe and effective as their brand-name counterparts.

What if my doctor says I need the brand-name drug?

If your doctor believes a brand-name drug is medically necessary-for example, because you had a bad reaction to the generic-you can request a coverage exception. Your doctor will submit paperwork explaining why. Your insurer will review it. If approved, they’ll cover the brand-name drug even if it’s not on the formulary. This is a common process and rarely denied for valid medical reasons.

Why did my drug suddenly get removed from my plan’s formulary?

Pharmacy Benefit Managers (PBMs) regularly update formularies based on negotiations with drugmakers. If a manufacturer doesn’t offer a big enough discount, the PBM may remove the drug to push for lower prices. Sometimes, a generic becomes available, and the brand gets moved to a higher tier. Changes can happen without notice, so it’s important to check your drug list regularly.

Do I have to use the generic version if it’s available?

No, you’re not forced to. But if you choose the brand-name drug when a generic is available, you’ll pay more-often significantly more. For example, you might pay $10 for the generic but $75 for the brand. The system is designed to encourage you toward the lower-cost option. You can still choose the brand, but you’ll be paying the difference.

How can I find out what drugs are covered by my plan?

Visit your health insurer’s website and look for your plan’s drug list or formulary. You can also check your Summary of Benefits and Coverage (SBC), which is required to be provided by your employer. If you’re unsure, call your insurer directly. They can tell you if your medication is covered, what tier it’s on, and what your copay will be.

peter vencken

March 26, 2026 AT 08:18man i just found out my insulin is in tier 4 and i’ve been paying $180 a month. turns out there’s a generic that’s $12. i asked my pharmacist and he looked at me like i was from another planet. why don’t more people know this? i’m telling everyone now.

Chris Crosson

March 26, 2026 AT 22:51the system works if you know how to play it. i used to take the brand-name blood pressure med until i checked my formulary. switched to generic, saved $65 a month. no side effects, no difference. why do people think brand = better? it’s marketing, not medicine.

Linda Foster

March 27, 2026 AT 11:23It is imperative that individuals take the initiative to review their Summary of Benefits and Coverage, as well as consult with their respective Pharmacy Benefit Managers, to ensure that they are fully informed regarding the parameters of their prescription coverage. This diligence facilitates optimal health outcomes and financial prudence.

Anil Arekar

March 27, 2026 AT 13:13As someone from India where generics are the norm, I find this system both logical and humane. In our healthcare system, generics are not just preferred-they are the foundation. The idea that cost-efficiency and efficacy can coexist is not foreign. Perhaps if more employers communicated this as clearly as public health systems do in developing nations, adoption would be far higher.

Rama Rish

March 28, 2026 AT 14:20generic work. i took the cheap one for my anxiety and nothin changed. why pay extra? my boss should send a text about this.

Kevin Siewe

March 29, 2026 AT 00:50I’ve worked in healthcare for 15 years, and I’ve seen firsthand how PBMs manipulate formularies. The GTN spread is real-it’s not just about savings, it’s about hidden profits. Employers think they’re cutting costs, but they’re often just letting middlemen profit more. Transparency is what’s missing here.

Chris Farley

March 31, 2026 AT 00:17So let me get this straight-we’re supposed to be grateful that corporations are forcing us to take cheaper drugs because they ‘saved’ $150 billion? Who the hell decided that my health should be a spreadsheet? This isn’t healthcare-it’s corporate cost-shifting disguised as efficiency. Next they’ll tell us to take aspirin for cancer.

Darlene Gomez

April 1, 2026 AT 03:44I love how this post ends with ‘you’re using the system the way it was designed to work.’ But the system was designed to protect profits, not patients. The fact that we’re praised for choosing the $10 generic instead of the $75 brand is a tragedy. We should be fighting for a system where cost isn’t a barrier to the best treatment-period. Generics are great, but they shouldn’t be the only option we’re allowed to have.

Elaine Parra

April 3, 2026 AT 00:40Why are we letting these PBMs decide what drugs we can take? This isn’t America. This is corporate feudalism. If you’re on a brand-name drug that works for you, you should be able to keep it without being punished financially. This is a betrayal of medical freedom. We’re not in China-we don’t need government-approved pill menus.

Katie Putbrese

April 4, 2026 AT 03:58I can’t believe people are okay with this. My cousin had to switch from her brand-name seizure med to a generic and had a seizure at work. Now she’s on disability. The FDA says they’re the same, but biology isn’t a spreadsheet. This system is dangerous, and anyone who defends it is ignoring real human suffering.

Natasha Rodríguez Lara

April 4, 2026 AT 06:43Just wanted to say-this is actually one of the clearest breakdowns I’ve seen. I’m a nurse in Ohio and I see this every day. Patients don’t understand tiers until you sit down with them. I’ve started handing out little printed guides at the clinic. One woman cried because she didn’t know she could’ve been paying $12 instead of $70 for six years. Knowledge really is power.